What does real estate have to do with public transportation? Actually, quite a lot.

From Michigan Central Station in Detroit to the Hudson Terminal, Helmsley Building, and Hotel Pennsylvania in NYC, American railroads of the 20th century maintained a profit partly due to the transportation hub real estate assets they developed, owned, leased, and/or maintained vis-a-vis value capture and joint development. But as (auto)mobility took over socially, economically, politically, and physically, these railroads could no longer compete. Government and market forces combined to suburbanize white people, divest from public transit, and build highways.

Detroit (ABOVE) and Dallas (BELOW)

Detroit, the Motor City, is antithetical to railroad terminals, so it is sadly fitting that Amtrak trains are rerouted from the city’s abandoned central station to an “Amshak“. However, the city has recently added commercial tenants to the Rosa Parks Transit Center. Meanwhile, Dallas has been building the DART Light Rail, hoping for a more lively downtown and for more infill.

ABOVE: Michigan Central Station in the Motor City…

ABOVE: The CBD People Mover and Detroit…

ABOVE: Dallas DART Light Rail Station (EMPTY SPRAWL SPACE!)

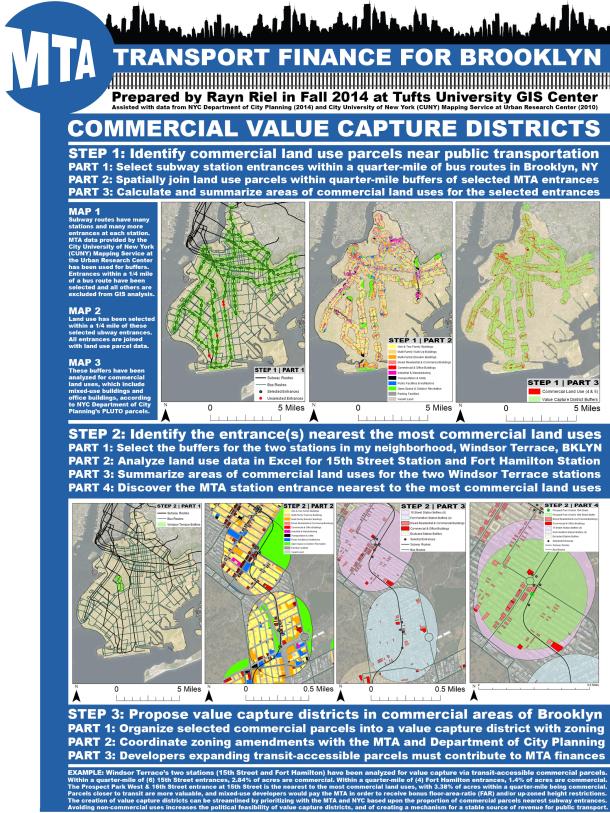

According to Levinson, Zhao, and Iacono (University of Minnesota), there are various tools and techniques that can be used in order to implement value capture. Special assessment districts levy an additional tax on land parcels that receive a direct benefit from transit. Transportation utility fees are fees assessed on beneficiaries of transit infrastructure based upon how likely these beneficiaries will be using transit, thereby, for instance, reflecting the building’s density or parking capacity. Tax increment financing is a tax policy that captures the incremental difference in tax revenue after construction of transit facilities, in order to pay for the financing costs. Development impact fees are one-time fees assessed to developments, and are determined formally through policy. Negotiated extractions also are one-time fees assessed to developments, but they are negotiated on a case-by-case basis. Joint development is a public-private partnership between a developer and a public agency. And, last but not least, air rights are the sale or lease of air rights above a transit facility. Often, these tools and techniques are used together in order to complete a project; for instance, a developer may be using tax increment financing in order to practice joint development, while using air rights in order to increase density bonuses.

Private railroads tried to stay afloat by selling air rights in the age of competitive air travel, thus creating Madison Square Garden above the contemporary Penn Station and the PanAm/MetLife Building above GCT in NYC. Their remaining real estate assets were also sold, with reverberations of these deals remaining today, as seen with the air rights controversies surrounding Grand Central Terminal, owned by Andrew Penson, and One Vanderbilt, a proposed skyscraper part of the East Midtown Rezoning.

Penn Station, NYC

The government agencies that now tend to operate (or contract out) public transportation have few incentives to remain revenue-positive or self-sufficient through real estate development, since they are largely dependent upon taxes and fares. They also may not have the authority to conduct real estate deals, nor the transit-oriented assets to do so in the first place. In New York, the MTA faces institutional barriers ranging from cultural inertia to an unhealthy relationship between the State, City, and MTA. The public authority also simply doesn’t own much land that could be commercially developed, besides atop train yards (i.e., Hudson Yards, Atlantic Yards, Sunnyside Yards, Penn Yards, Terminal City), which is quite expensive. After all, trains must be kept operational while construction occurs above them.

Sunnyside Yards, Queens

Develop Jamaica Station in Queens!

However, the MTA does have spaces within some of its station concourses and abandoned passageways for retail vis-a-vis joint development. Still, even when the MTA has space for retail, as in the Fulton Center, they fail to seek revenue-positive opportunities. The Fulton Center is located in Lower Manhattan, and it is only a few stories tall with relatively few shops, so as to allow light to enter through the roof. Even if there was no demand for office space, the MTA could have sold air rights, or allowed for a developer to build transit-oriented housing, while still designing creatively, so light can flow into the concourse. Why didn’t they do this? They don’t have the incentives to do so.

Clearly, the need for state-sponsored reform is great, but it is a challenge for reform to occur, as evident through the recent attempt to reform the Port Authority by NY/NJ legislatures, as well as the lackluster MTA Reinvention Commission. Even though the MTA owns few assets, perhaps they could work with the City of New York in order to establish a zoning bonus allowing for increased FAR if developers chip into a stable MTA value capture fund. For example, the Second Avenue Subway is bound to increase the value of nearby properties, but there is no mechanism allowing for some of this increased value to be “captured” for continued investment. The city has been re-zoning locations near subway entrances for transit-oriented development, including ground-floor retail, mixed-income housing, and offices. Developers are able to build higher and increase their floor-area-ratio (FAR) due to transportation accessibility, but oftentimes, they do not need to contribute to the MTA’s revenue. If new incentives were to be formalized, including FAR bonuses for contributing to the renovation of a nearby station, then the MTA could be provided with a relatively stable source of income. American examples of value capture will help to catalyze the growth of this fiscally responsible practice in the U.S.

Indeed, MTA CEO Tom Prendergast states:

“I do believe it’s important that we get a menu of different funding sources up there that are sustainable. Sustainable in terms of the revenue they bring, and sustainable in terms of their long-term. In the sine-wave cycle that some of these revenue sources have, you hopefully have ones that are in a peak while others are in a valley. Value capture on real estate, there’s different elements of it, different cuts of it, but the idea of Seven West funding, where New York City is giving us [money] to fund the 7 Line is an example of that. There are cases, you can read Crain’s, as recently as 6 months ago, where someone bought a piece of property directly adjacent to the current phase one of the Second Avenue Subway, and they’re selling that property at increased value because of the investment that the MTA and the region is putting into the construction of the second avenue subway. It’s reasonable to expect that some of those profits should be shared by the people who actually made the improvements to the infrastructure and replow those revenues to further increases in the infrastructure network. The other one is cap and trade.” - MTA CEO Tom Prendergast

MTA’s former CEO, Jay Walder, would definitely be able to help, too. He left the MTA in order to work for the MTR Corporation in Hong Kong, one of the world’s only profitable public transportation companies. While no longer working in Hong Kong, he’s chimed in on this issue multiple times, as reported in this informative article. The MTR’s Rail+Property Program may not be able to be ‘transported’ to New York City due to astronomically higher operation and construction costs, as well as a lack of government-owned land. Yet, even when presented with an opportunity (such as the Fulton Center), the MTA chose to develop a four-story hub in the heart of Lower Manhattan. While it’s designed beautifully, it lacks value capture.

Fulton Center, NYC

While the indebted Port Authority (and PATH) in NY/NJ is legally self-sufficient, relying on tolls, fares, and real estate revenue (WTC, Bus Terminal, JFK, LGA, EWR), it is far from self-sufficient. Nevertheless, it is not like the MTA, which relies on taxes, fares, and “TBTA” tolls. And the MTA is not the MTR, which is a profitable and privatized corporation, largely owned by government shareholdings in Hong Kong. This system works in Hong Kong because the government is relatively centralized and land ownership laws are not as individually-oriented as in the United States. It also works because Hong Kong is one of the densest cities on the planet, and the MTR feeds people into its transit-oriented malls, apartments, and offices. The MTR’s sustainable financial model integrates living, working, and playing into interconnected T.O.D. neighborhoods. The MTR typically owns property below ground, including countless retail outlets, and it will work with developers to sell, lease, or manage property atop its stations, including the tallest buildings of Hong Kong: International Finance Centre on Hong Kong Island and International Commerce Centre in Kowloon.

MTR Property on Hong Kong Island (RIGHT)

MTR Construction in Kowloon

MTR Station & Mall Entrance in ICC Kowloon Master-Plan Community

Apartments Atop MTR Train Yard

Apartments Atop Tsing Yi MTR Station

MTR Malls: Maritime Square (Tsing Yi)

MTR Shops: Hong Kong Station

Typical MTR Underground Shopping

MTR IFC Mall (Allowing light into the station whilst practicing joint development)

Density in Hong Kong (Above and Beyond…)

New York State’s public transportation network is the most heavily used and developed in the United States. Yet the state and its numerous authorities and municipalities have never been able to establish a stable funding strategy for the MTA. The Hudson Yards was financed by commercial development, with 28 million square feet of new offices planned by 2035. The MTA’s extension was financed by New York City, and with additional property taxes providing nearly half of the revenue raised through value capture. This may not be possible elsewhere unless zoning is changed to allow for increased T.O.D. density, so new buildings can have a tremendous impact on funding. Currently, many of the MTA’s stations are also in dense areas of the city, and these stations could potentially be retrofitted with retail, but self-sufficiency would not be possible. Even still, additional revenue never hurts, as seen with the MTA’s shopping options at Grand Central Terminal, or the independent South Ferry Plaza Proposal.

Hudson Yards, NYC

What can be done about bureaucratic regulations and contracts, public unions, disincentives, a lack of opportunity sites and market potential for mixed-use revenue-generation, and a lack of collaboration with the City of New York and New York State? How can the MTA traverse barriers towards joint development and value capture mechanisms? They can begin by selling air rights at the Fulton Center and exploring retail opportunities in their stations (and at the Low Line). Long-term changes could involve institutional changes at the MTA and in Albany, as well as the development of a value capture zoning district mechanism.

Here is my GIS proposal for an MTA value capture district:

The Taipei Metro (MRT) has a Metro Mall, Singapore’s MRT is renowned for T.O.D., and in Dubai, the Roads and Transport Authority (RTA) is working on a joint development project atop the Union Square Metro Station, complete with air conditioned towers for businesses, restaurants, offices, and residences. They are even creating a public-private partnership for the property, which spans 19,000 square meters. To me, this seems a lot more practical than the Masdar Personal Rapid Transit (PRT) system in Abu Dhabi, which has been cancelled. Maybe the UAE is realizing the importance of public transit…

Yet a renewed MTA would be a model for other American networks, from the Boston MBTA (Beacon Park Yard and South Station) to the Transbay Center in San Francisco. Perhaps it would also inspire Juneau, the capital of Alaska, to design itself as a car-free city; after all, it’s already not connected via roads to anywhere else in Alaska. It would also be a renewed New York, able to compete in the 21st century. It may never be profitable like the MTR or Tokyo’s private subways, but it should nevertheless maximize revenue at existing assets…

Assembly Row (MBTA Orange Line), Somerville, MA (Supposedly T.O.D…)

South Station, Boston, MA

Transbay Center, San Francisco

Dense Retail at Tokyo Station, Japan

This post is a “preliminary introduction” to my IRB approved Senior Honors Thesis research at Tufts University and part of a series of posts related to the subject. Many thanks to my New York and Hong Kong interviewees thus far for sharing their time and expertise, including an anonymous city official, as well as Robert Paaswell, Subutay Musluoglu, Jason Fane, Dan Peterson, Dorothy Chan, and Sai Ping Chin. Interviews with MTA officials are TBD! Also, additional gratitude to the Undergraduate Research Fund for assisting with research expenses.

All photos are taken by Rayn Riel.

Summary: New York’s Metropolitan Transportation Authority (MTA) is constantly running trains, but it is also constantly running a deficit. Unlike profitable transportation companies, such as the Hong Kong MTR, the MTA has few valuable real estate assets which could be adequately transformed into transit-oriented joint development hubs. Akin to other U.S. public transportation agencies, space for pragmatic and profitable commercial activities – including shops and offices operating on agency-owned land – is limited to a few select stations, yards, concourses, and passageways. However, while the MTA’s ability to remain revenue-positive or self-sufficient through real estate development is impossible, the MTA could nevertheless capitalize upon its few existing assets for additional revenue. The MTA could also work with the City of New York to develop a value capture mechanism in mixed-use commercial districts accessible by subway and bus routes. The MTA increases real estate values, which means higher taxes and fees, but this revenue is not shared back with the MTA. This Senior Honors Thesis will elucidate how the MTA can contextually transport value capture and joint development practices from abroad and overcome organizational barriers in order to ‘transport’ the MTA’s limited portfolio of assets into ‘transformation hubs’. While there is ‘room’ for improvement, institutional barriers ranging from cultural inertia to an unhealthy relationship between the City, State, and MTA would need to be transcended through coordinated reformation efforts.

PS: http://www.globes.co.il/en/article-israel-railways-reports-first-ever-profit-1000998854

LikeLike

Checking to see if a transfer of development rights (TDR) is feasible for the Fulton Center. If anyone knows, please feel free to share!

LikeLike

In Hong Kong, the MTR is a profitable, privatized transportation company. They develop some of the city’s tallest skyscrapers. They build housing atop almost all of their stations. They own, operate, and maintain malls. This works because Hong Kong is a dense and self-contained Special Administrative Region. It is very difficult to own a car. Thus, ridership fuels the MTR’s profitability, and the MTR builds transit-owned developments, thereby fueling ridership even more, in a positive feedback loop of density and dynamism. And as a privatized company, the MTR has a profit motive, and they have ample incentives to develop property. Furthermore, China’s land ownership laws allow for the central government to, essentially, lease the MTR land to develop. We cannot easily ‘transport’ this transportation model to American cities.

Our cities are less dense, our subways have fewer riders. Thus, an ‘MTR Mall’ would not be able to be successful in most of our country’s subterranean stations. (Except for, largely, stations in Manhattan).

Here in Baltimore, I’ve taken a few photos…

LikeLike

Baltimore Light Rail

LikeLike